Mutual Funds vs ETFs vs Index Funds: Key Differences Every Beginner Should Know

Mutual Funds vs ETFs vs Index Funds: Key Differences Every Beginner Should Know

When you first start researching how to invest, three terms appear constantly: mutual funds, ETFs, and index funds.

They sound similar. They are often compared together. And the differences between them confuse a significant number of new investors — which sometimes leads to decision paralysis and not investing at all.

This guide will clear up the confusion completely.

By the end, you will understand exactly what each one is, how they differ, what they cost, and which one makes the most sense for your situation as a beginner investor.

First: Understanding the Basic Categories

Before comparing, it helps to understand how these terms relate to each other.

Mutual fund and ETF describe the structure of a fund — how it is packaged and traded.

Index fund describes the strategy — whether a fund passively tracks an index or is actively managed.

This means:

- An index fund can be structured as a mutual fund

- An index fund can also be structured as an ETF

- A mutual fund can follow an index (passive) or be actively managed

- An ETF can follow an index or be actively managed

The confusion comes from people using these terms loosely. In common usage, “index fund” often refers specifically to a low-cost mutual fund that tracks an index (like those offered by Vanguard or Fidelity). But technically, any fund that tracks an index — regardless of structure — is an index fund.

Here is a simple diagram to visualize this:

All Funds

├── Mutual Funds

│ ├── Index Mutual Funds (passive — tracks an index)

│ └── Actively Managed Mutual Funds

└── ETFs (Exchange-Traded Funds)

├── Index ETFs (passive — tracks an index)

└── Actively Managed ETFs

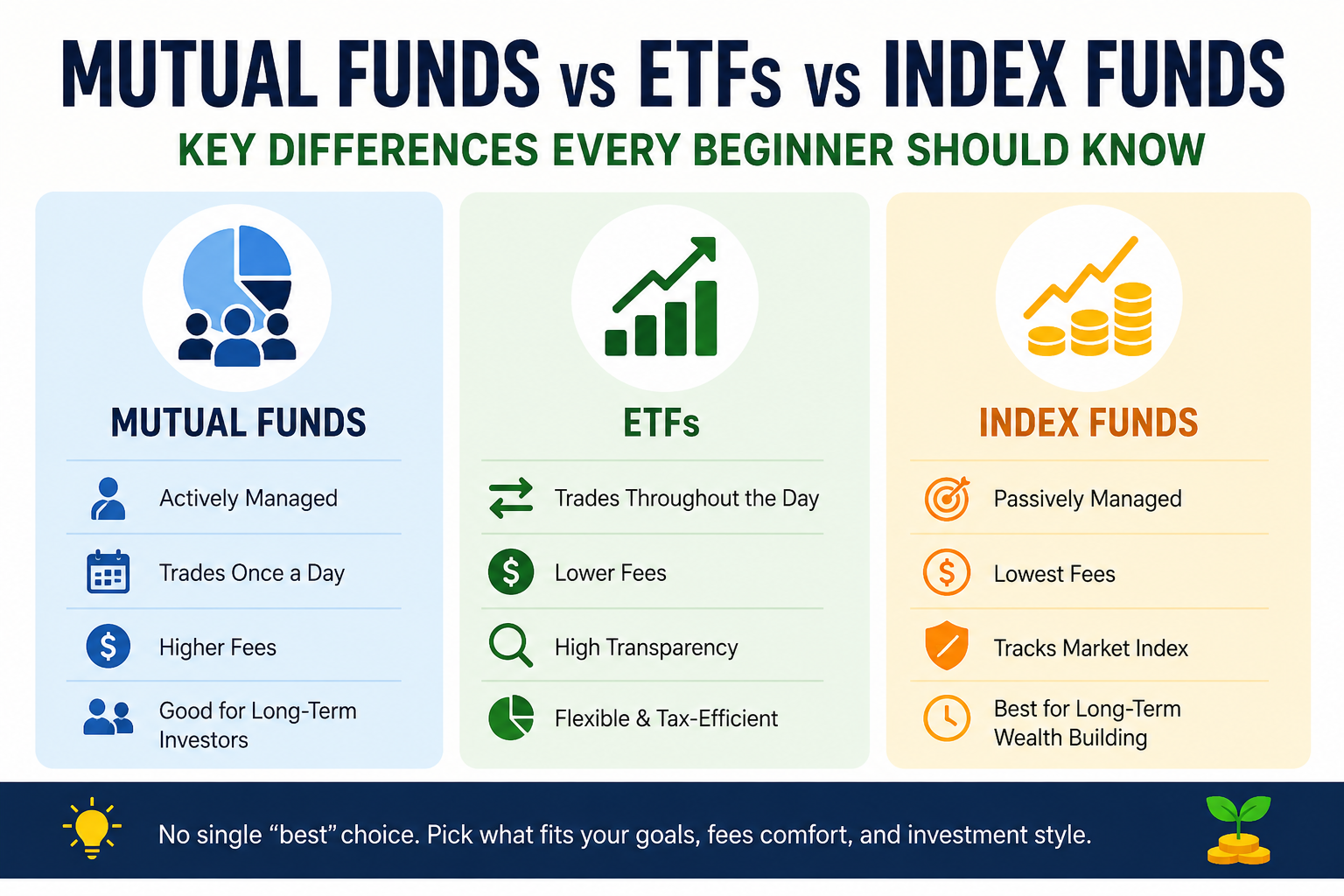

What Is a Mutual Fund?

A mutual fund pools money from many investors to buy a collection of assets — stocks, bonds, or both.

Key characteristics:

- Pricing: Priced once per day, after markets close (Net Asset Value / NAV)

- Trading: Bought and sold directly through the fund company, not on a stock exchange

- Minimums: Often have minimum investment requirements ($500, $1,000, or more — though many now offer $0 minimums)

- Management: Can be actively managed (fund manager picks investments) or passively managed (tracks an index)

- Dividends: Automatically reinvested or paid out — depends on settings

Types of mutual funds:

- Actively managed — A professional fund manager makes investment decisions

- Index mutual funds — Passively tracks a market index with no active decision-making

Mutual funds are the older, more traditional structure. They have been available to retail investors since the 1920s and remain the dominant vehicle in employer-sponsored retirement accounts like 401(k)s.

What Is an ETF?

An ETF (Exchange-Traded Fund) is a fund that trades on a stock exchange throughout the day — just like an individual stock.

Key characteristics:

- Pricing: Priced continuously throughout the trading day (market price fluctuates)

- Trading: Bought and sold on stock exchanges through a brokerage account

- Minimums: No minimum beyond the price of one share (and fractional shares are widely available)

- Management: The vast majority of ETFs are passive index funds, though actively managed ETFs exist

- Dividends: Paid out to investors (reinvestment depends on brokerage settings)

ETFs were introduced in the early 1990s and have grown rapidly in popularity. Their combination of low costs, trading flexibility, and accessibility has made them the preferred investment vehicle for many individual investors.

What Is an Index Fund?

An index fund is any fund — mutual fund or ETF — that passively tracks a specific market index.

Instead of paying a fund manager to pick stocks, an index fund simply buys all (or a representative sample of) the securities in its target index and holds them. When the index changes its composition, the fund adjusts accordingly.

Key characteristics:

- Strategy: Passive — no active stock picking

- Cost: Typically very low expense ratios (0.03%–0.20%)

- Performance: Historically outperforms most actively managed funds over long periods

- Transparency: Holdings always known and predictable

- Structure: Can be either a mutual fund or an ETF

The term “index fund” in common usage typically refers to low-cost index mutual funds from providers like Vanguard, Fidelity, and Schwab — particularly in retirement account contexts.

Head-to-Head Comparison

| Feature | Mutual Fund (Active) | Index Mutual Fund | Index ETF |

|---|---|---|---|

| Management style | Active | Passive | Passive |

| Expense ratio | 0.5%–2%+ | 0.03%–0.20% | 0.03%–0.20% |

| Trading | Once daily (NAV) | Once daily (NAV) | Throughout day |

| Minimum investment | Often $500–$1,000+ | Often $0–$1,000 | Price of 1 share (or fractional) |

| Performance vs market | Usually underperforms long-term | Matches market | Matches market |

| Tax efficiency | Lower | Moderate | Higher |

| Best for | Specific strategies (rarely) | Retirement accounts | Taxable accounts, beginners |

| Flexibility | Low | Low | High |

The Fee Difference — Why It Matters So Much

The most practically important difference between actively managed mutual funds and index funds (whether mutual fund or ETF) is cost.

Actively managed mutual fund: Typically 0.5%–2% expense ratio annually Index fund (ETF or mutual fund): Typically 0.03%–0.20% annually

This seems small. But compounded over decades, the gap is enormous.

$10,000 invested for 30 years at 8% gross annual return:

| Fund Type | Expense Ratio | Final Value |

|---|---|---|

| Index ETF | 0.03% | ~$99,300 |

| Index Mutual Fund | 0.10% | ~$97,900 |

| Active Mutual Fund (low) | 0.75% | ~$85,700 |

| Active Mutual Fund (high) | 1.50% | ~$74,500 |

| Expensive Active Fund | 2.00% | ~$66,100 |

The difference between a 0.03% ETF and a 2% active fund over 30 years is over $33,000 — from the same starting investment, at the same gross return. That gap is entirely created by fees.

This is the core reason most financial educators recommend low-cost index funds and ETFs over actively managed mutual funds for long-term investing.

Which One Actually Performs Better?

The evidence on this question is extensive and fairly consistent.

The SPIVA (S&P Indices Versus Active) report — published by S&P Dow Jones Indices — tracks how actively managed funds perform against their benchmark index over various periods. Consistently across multiple years and markets, the majority of active funds underperform their benchmark index over 10 and 15-year periods after fees.

This does not mean every active fund underperforms. Some do beat the market. But identifying which ones will outperform in advance is extremely difficult — and past performance does not reliably predict future results.

For long-term investors, the mathematically consistent approach is to own the market through low-cost index funds rather than try to beat it through active management.

When Might an Actively Managed Fund Be Appropriate?

In the interest of balance — there are specific situations where actively managed funds may have merit:

- Niche or illiquid markets where passive indexing is difficult (some emerging markets, private credit)

- Specific strategies not available through index funds (certain hedging strategies, alternative investments)

- Institutional investors with access to genuinely differentiated managers

For the vast majority of individual investors — particularly beginners — these situations do not apply. Low-cost index funds remain the better starting point.

ETF vs Index Mutual Fund — Which Should You Choose?

For most beginners, the choice between an index ETF and an index mutual fund is less important than simply choosing low-cost, broadly diversified funds. Both are excellent options.

Here is when each tends to work better:

Choose Index ETFs when:

- You are investing in a taxable brokerage account (ETFs are generally more tax-efficient)

- You want to invest with no minimum — fractional shares available

- You prefer trading flexibility throughout the day

- You are using a platform that offers commission-free ETF trading

Choose Index Mutual Funds when:

- You are investing through a 401(k) or retirement account where mutual funds are the primary option

- You want automatic dividend reinvestment handled seamlessly

- You prefer simple round-dollar contributions without worrying about share prices

For the best platforms to access both: Best Investment Apps 2026

How This Connects to Your Overall Investment Strategy

Understanding these fund types is an important foundation, but it fits into a broader investment picture.

The typical beginner investor path:

- Build emergency fund → How to Build an Emergency Fund in 2026

- Eliminate high-interest debt → Debt Snowball vs Debt Avalanche

- Start investing in low-cost index funds → this article

- Use Dollar Cost Averaging for consistent contributions → DCA Strategy Complete Guide

- Let compound growth work over time → Compound Interest Calculator

- Build toward financial independence → Build Wealth From Scratch

Each step connects to the next. Understanding what you are investing in — and why — makes every step more confident and more effective.

Practical Starting Points for Beginners

If you are ready to invest and want a concrete starting point:

Option A — Simple One-Fund Approach: Choose a total market index ETF (like VTI — Vanguard Total Stock Market ETF) or equivalent in your country. Invest whatever you can monthly. Done.

Option B — Two-Fund Portfolio: US total market index fund + International index fund. Provides US and global diversification in two simple holdings.

Option C — Three-Fund Portfolio: US total market + International + Bond index fund. Adds some stability through bonds. Good for investors approaching retirement or with lower risk tolerance.

Note: Always verify fund availability, fees, and regulatory status in your country before investing.

Quick Reference: Key Terms

| Term | Simple Definition |

|---|---|

| Mutual Fund | A pooled investment fund bought/sold once daily through the fund company |

| ETF | A fund traded on a stock exchange throughout the day like a stock |

| Index Fund | Any fund that passively tracks a market index (low cost, no active management) |

| Expense Ratio | Annual fee charged by a fund as % of your investment |

| Active Management | A fund manager picks investments trying to beat the market |

| Passive Management | Fund automatically mirrors an index — no stock picking |

| NAV | Net Asset Value — the per-share value of a mutual fund calculated daily |

| Fractional Shares | Buying a portion of one share — allows investing any dollar amount |

| Dividend | Payment made to shareholders from company profits |

People Also Ask

Q: What is the difference between a mutual fund and an ETF? Both are pooled investment funds. The key differences are how they trade (mutual funds once daily, ETFs throughout the day on an exchange), their minimum investment requirements (ETFs often have lower minimums), and their tax efficiency (ETFs are generally more tax-efficient in taxable accounts).

Q: Is an index fund the same as an ETF? Not exactly. An index fund describes a strategy (passive, tracks an index), while an ETF describes a structure (trades on an exchange). Most ETFs are index funds, and index funds can be structured as either ETFs or mutual funds.

Q: Which is better — an ETF or a mutual fund? For most individual investors in taxable accounts, low-cost index ETFs are slightly preferable due to lower minimums, tax efficiency, and flexibility. In retirement accounts like 401(k)s, index mutual funds are often the primary option and are equally effective.

Q: Why do actively managed funds underperform index funds? Primarily because of fees. Active fund managers charge higher fees to cover their research and management costs. These fees create a consistent drag on returns that most active managers cannot overcome through stock selection, particularly over long periods.

Q: What is an expense ratio? An expense ratio is the annual fee a fund charges, expressed as a percentage of your investment. A 0.03% expense ratio costs $3 per year on $10,000. A 1.5% ratio costs $150. Over decades, this difference compounds into significantly different outcomes.

Q: Can I lose money in an index fund? Yes. Index funds reflect the performance of their underlying market. When markets fall, index funds fall too. They can drop 20–40% in major market downturns. However, over long periods, broadly diversified index funds have historically recovered and grown beyond previous levels.

Q: How do I choose between an index ETF and index mutual fund? In a taxable account, index ETFs are generally more tax-efficient. In a retirement account like a 401(k), index mutual funds are typically your main option. Both are excellent vehicles. The fund’s expense ratio and the underlying index it tracks matter more than the structural difference.

Q: What is the minimum investment for an ETF? Most ETFs can be purchased for the price of one share. Many brokerages now offer fractional shares, meaning you can invest as little as $1 in virtually any ETF.

⚠️ Investment Disclaimer: This article is for educational and informational purposes only. All investments carry risk including the potential loss of principal. Past performance does not guarantee future results. The funds and platforms mentioned are examples for illustrative purposes only — always verify current fees, details, and availability in your country directly with the provider. This article does not constitute personalized investment advice. Please consult a qualified financial advisor before making investment decisions. Finzaro360.com does not provide personalized investment advice.

Conclusion

The mutual fund vs ETF vs index fund comparison is simpler than it first appears once you understand how the terms relate.

Mutual fund and ETF describe how a fund is structured and traded. Index fund describes whether it is passively managed or actively managed.

For most beginner investors, the practical conclusion is straightforward: choose low-cost, passively managed index funds — whether structured as ETFs or mutual funds — over actively managed funds. Keep fees low, diversify broadly, invest consistently, and give your investments time to compound.

The structural details matter less than the habit of consistent, low-cost, diversified investing over the long term.

Start simple. Stay consistent. Let time do the heavy work.

What to Read Next on Finzaro360

- Index Funds for Beginners: The Complete Guide 2026

- How to Invest With Little Money: Start With $100 or Less

- DCA Strategy — Dollar Cost Averaging Complete Guide

- Compound Interest Calculator: How It Works & Why It Changes Everything

- Best Investment Apps 2026

- Build Wealth From Scratch: Saving, Investing & Smart Money Habits

Write for Finzaro360

Are you a finance or investing expert? We publish guest posts on Finance, Crypto, AI Tools, and Online Earning topics. Visit our Write For Us page to submit your pitch and earn a quality dofollow backlink.

Published on Finzaro360.com | Category: Finance