The 50/30/20 Budget Rule Explained for Beginners: Save Money & Build Financial Freedom

The 50/30/20 Budget Rule:

Save Money & Build Financial Freedom

The simplest, most powerful budgeting method ever created — explained in plain English for real people with real struggles.

The Money Struggle Nobody Talks About

Let me ask you something honest: does your salary disappear before the month is over?

You’re not careless. You’re not bad with money. You’re just living in a world where everything costs more, salaries haven’t kept pace with inflation, and nobody ever taught us how to actually budget. Not in school. Not at home. Not anywhere.

Families today are stretched thin between rent, groceries, school fees, phone bills, and the occasional emergency that always arrives at exactly the wrong time. Students are juggling tuition and basic survival. Salaried professionals feel trapped in a cycle where earning more somehow never seems to lead to saving more.

That’s where the 50/30/20 budget rule comes in. It’s beautifully simple. It’s been proven across millions of households. And it might be the single most life-changing financial concept you’ll learn today.

In this guide, we’ll break it all down — what it means, how to actually use it, real-world examples, common traps to avoid, and the tools that make it easier. Whether you’re a student managing a small income, a parent trying to keep the household afloat, or a professional who simply wants to stop living paycheck to paycheck — this guide is for you.

Let’s start. Your financial future deserves this conversation.

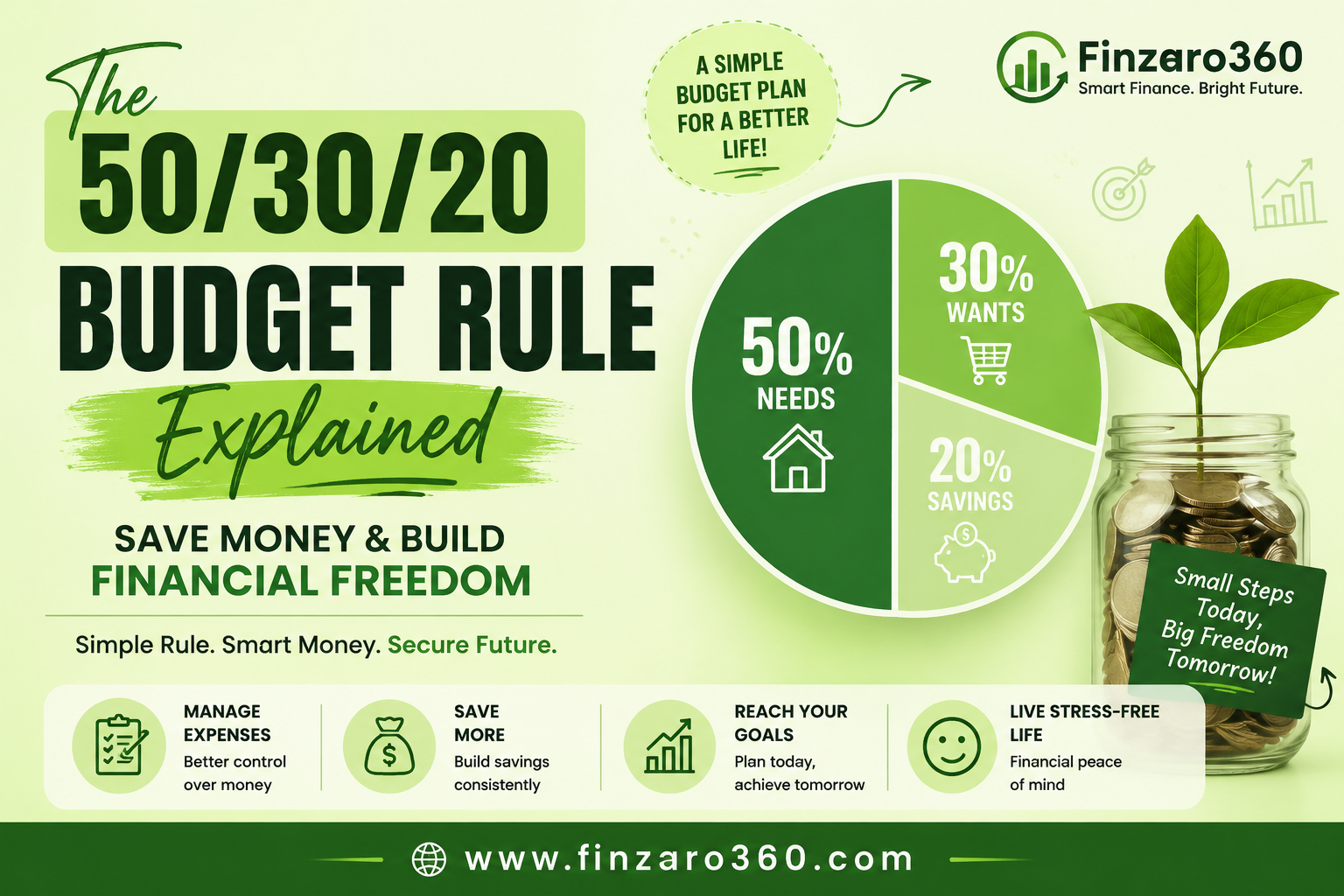

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple personal budgeting framework that divides your after-tax income into three clearly defined categories: Needs, Wants, and Savings.

It was popularized by U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their landmark book All Your Worth: The Ultimate Lifetime Money Plan. Their research showed that the biggest financial predictor of long-term security wasn’t how much people earned — it was how they divided what they earned.

That’s the entire framework. Three buckets. No spreadsheets with 47 categories. No guilt over every coffee purchase. Just three numbers: 50, 30, 20.

What makes this rule so powerful is its flexibility. It’s a guideline, not a rigid prison. If your city has high rent, maybe your needs are 60% — that’s okay, the framework adapts. If you’re aggressively paying off debt, you might push savings to 30%. The structure gives you a starting point and a direction.

Want to explore even more budgeting tips beyond this rule? There are many strategies that complement the 50/30/20 framework beautifully — but for most people, this rule alone is enough to transform their relationship with money.

How It Works: Step-by-Step

Understanding the concept is one thing. Actually applying it is another. Here’s exactly how to set up the 50/30/20 rule for your life — starting today.

Calculate Your After-Tax Monthly Income

This is your take-home pay — what actually lands in your bank account after taxes, pension contributions, and any other deductions. If you’re a freelancer or self-employed, estimate your average monthly earnings after setting aside taxes. Use your consistent, reliable income — don’t count bonuses or irregular payments at this stage.

Identify Your “Needs” (50%)

Needs are expenses you genuinely cannot avoid. These include: housing costs (rent or mortgage), utility bills, groceries, essential medication, minimum debt payments, and transportation to work. A helpful test: “If I didn’t pay this, would something essential stop working or would I face serious consequences?” If yes — it’s a need. If no — it’s likely a want.

Define Your “Wants” (30%)

Wants are the things that make life enjoyable but aren’t survival essentials. Think: dining out, streaming subscriptions, gym memberships, weekend trips, new clothes beyond basics, hobbies, and entertainment. This doesn’t mean wants are bad — they’re an important part of a balanced, sustainable budget. A budget that allows zero joy is a budget nobody keeps.

Commit to Saving & Investing (20%)

This is where your future self lives. The 20% savings bucket covers: emergency fund building, retirement contributions, investment accounts, and accelerated debt repayment (beyond minimums). The key principle here is to pay yourself first — transfer this amount the day your salary arrives, before you have a chance to spend it. Automate this if at all possible.

Track, Review, and Adjust Monthly

At the end of every month, review what actually happened versus your plan. Did needs creep over 50%? Was your savings really 20% or did you “borrow” from it? This monthly review is where real financial growth happens — not in the planning, but in the honest looking. Check out our financial planning guide for a complete monthly review system.

Open three separate bank accounts — one for needs, one for wants, one for savings. When your salary arrives, immediately transfer the right percentages. This removes willpower from the equation entirely. You can’t accidentally spend your savings if it’s sitting in a different account you don’t touch.

Real-Life Examples: Making It Personal

The Salaried Professional

Imagine someone working a desk job in a mid-sized city. They bring home a decent monthly salary — enough to live on, not enough to feel comfortable. Every month, more goes out than planned. Sound familiar?

Applying the 50/30/20 rule gives this person a clear picture for the first time: roughly half their income goes to rent, groceries, and transport. About a third covers the lifestyle expenses — the Friday dinners, the occasional new pair of shoes, the streaming services. And the remaining fifth gets directed, consistently, toward an emergency fund and a retirement account.

Six months into this system, they have their first real financial cushion. That cushion is what separates people who panic at a car repair from people who handle it calmly. That cushion is the beginning of financial freedom.

The Young Family

A couple with one child often feels like the walls are closing in financially. Childcare alone can feel like a second rent. The 50/30/20 framework forces an honest conversation: which of their current expenses are truly needs, and which have quietly become habits? Often, families discover they’ve been spending much more on wants (delivery apps, premium subscriptions, impulse buys) than they realized — and that small adjustments free up real money for savings.

For families, the savings bucket is especially important. Emergency funds protect against the unexpected medical bill or job disruption. Long-term savings protect the children’s future. Read more about family strategies to save money fast that specifically address the financial pressures families face.

The Student on a Tight Budget

Students often feel budgeting doesn’t apply to them because “there’s nothing to budget.” But even with limited income — part-time work, an allowance, or a small scholarship — the 50/30/20 framework builds habits that compound dramatically over time. A student who saves even a small percentage of their income in their early twenties understands money in a way their peers simply don’t. That understanding is worth more than any individual sum saved.

The goal of the 50/30/20 rule isn’t perfection. It’s intentionality. When you choose to spend, when you know where every unit of your income is going, you stop feeling out of control. That feeling — of being the one deciding what happens with your money — is the first real step toward financial freedom.

Pros & Cons of the 50/30/20 Rule

No budgeting method is perfect for everyone. Here’s an honest look at what makes this rule excellent — and where it can fall short.

- Extremely simple — takes minutes to set up

- Flexible enough to adapt to any income level

- Doesn’t require obsessive tracking of every expense

- Prevents the “I’ll save whatever is left” trap

- Creates guilt-free spending within the Wants category

- Encourages consistent saving without complexity

- Works for individuals, couples, and families

- Easy to review and course-correct monthly

- Can be hard in high cost-of-living cities where needs exceed 50%

- Doesn’t address specific debt payoff strategies

- 30% Wants feels high for those in aggressive savings mode

- Not detailed enough for people with complex finances

- May need significant adjustment for very low incomes

- Doesn’t specify how to invest the 20% savings

The bottom line: for most people, especially beginners, the 50/30/20 rule’s simplicity is a feature, not a limitation. A perfect budget you never use beats a complex one you abandon after two weeks.

50/30/20 vs 70/20/10: Which Rule Is Right for You?

You may have come across another popular framework — the 70/20/10 rule. It allocates 70% to living expenses (needs + wants combined), 20% to savings, and 10% to giving or debt. Here’s how the two systems compare across different life situations:

| Factor | 50/30/20 Rule | 70/20/10 Rule |

|---|---|---|

| Structure | Separates Needs vs Wants explicitly | Combines living expenses into one bucket |

| Best for: Low Income | Challenging — 50% needs may not be realistic | Better fit — more flexibility in the 70% bucket |

| Best for: Middle Class | Excellent — clear categories, strong savings discipline | Works, but less structure on wants vs needs |

| Best for: Students | Great — teaches spending discipline from day one | Also works — simpler if income is very irregular |

| Best for: Families | Strong — clear savings mandate protects the future | Moderate — giving/tithing is a plus for some families |

| Best for: High Earners | Adapt needed — 30% wants feels high; increase savings % | Same — consider custom splits at higher incomes |

| Complexity | Very simple | Simple, but less granular |

| Savings Rate | 20% (can push to 20–30%) | 20% (identical base rate) |

| Includes Giving | Optional (from savings or wants) | Yes — explicit 10% category |

Our Verdict

For most beginners and middle-income households: the 50/30/20 rule wins because it forces a critical distinction between needs and wants — awareness that alone changes financial behavior. For lower incomes: the 70/20/10 rule offers more realistic breathing room. For anyone religious or community-oriented: the 70/20/10’s built-in giving percentage may resonate more deeply.

Neither rule is universally superior. The best budget rule is the one you will actually follow.

Common Mistakes People Make (And How to Avoid Them)

Mistake 1: Applying the Rule to Gross Income

The 50/30/20 rule works on your take-home (after-tax) income only. Using your gross salary inflates all three categories and sets you up to overspend. Always start from what actually enters your bank account.

Mistake 2: Mislabeling Wants as Needs

This is the most common and most honest mistake. A premium cable package is a want. A restaurant meal is a want. A second car (when public transport exists) may be a want. When needs consistently exceed 50%, the first question to ask is: “Am I calling wants by the wrong name?” Sometimes the answer is genuinely yes — your city is expensive and needs really are high. But sometimes, honest reflection reveals things that crept into the needs column they don’t belong in.

Mistake 3: Treating Savings as Optional

The most financially damaging habit: saving “whatever is left.” There is never anything left if you don’t protect it first. Transfer your 20% savings the day your income arrives. Make it non-negotiable. This single behavior change is responsible for more wealth-building than any investment strategy.

Mistake 4: Never Reviewing or Adjusting

Life changes. A new baby, a job loss, moving cities, a salary increase — all of these change your numbers. The 50/30/20 rule is a living system. Review it every month. Adjust when life requires it. Check our financial planning guide for a complete monthly review checklist.

Mistake 5: Comparing Your Budget to Others

Your colleague might be spending lavishly on wants and looking fine from the outside. You don’t see their debt, their anxiety, their 3am financial panic. Budget for your life, your goals, your future. Building wealth quietly and sustainably beats looking wealthy for an audience.

Inflation has made the “Needs” category harder to manage for many households in recent years. If you genuinely cannot keep needs under 50%, don’t abandon the framework — instead, focus your energy on either increasing income or finding one or two specific areas where needs can be reduced. Small, consistent cuts to fixed expenses (renegotiating bills, refinancing, moving to a more affordable area) compound significantly over time. See our guide on how to save money fast for practical ideas.

Protect Your Financial Life Online

Here’s something your bank won’t tell you: the greatest threat to your personal finances today isn’t overspending — it’s what happens to your financial data when you’re online.

Think about it. You check your bank balance on your phone at a café. You transfer money on a public network. You research investments, log into financial apps, shop for deals — all online. And in every one of those moments, without the right protection, your data can be exposed to people who would love to have it.

Cybercriminals increasingly target financial accounts, not banks. They target you — the individual whose login is transmitted over an unsecured network, whose online activity is tracked and sold, whose identity can be pieced together from browsing patterns alone.

NordVPN — Your Digital Privacy Layer

A VPN (Virtual Private Network) encrypts your internet connection, hides your IP address, and protects your online activity from hackers, data brokers, and surveillance — especially on public Wi-Fi networks.

Who particularly needs this:

- Freelancers and remote workers accessing company finances on the go

- Students using campus or café Wi-Fi for banking and payments

- Online earners, traders, and crypto users who handle sensitive financial transactions

- Anyone who shops online or uses financial apps on mobile

- Families who want to protect their household’s digital footprint

NordVPN is consistently rated among the fastest and most trusted VPNs available — with military-grade encryption, a verified no-logs policy, and coverage across all your devices simultaneously.

You work hard for your money. Protecting it online isn’t optional anymore — it’s part of smart financial management. A VPN subscription costs far less than the average cost of identity theft recovery.

Explore NordVPN Protection →* Affiliate disclosure: We may earn a commission if you subscribe through our link, at no extra cost to you. We only recommend tools we believe genuinely benefit our readers.

Shop Smarter, Save More

There’s a common misconception that frugal people don’t shop. In reality, financially smart people shop better — not less. The goal isn’t to deprive yourself; it’s to get genuine value for every currency unit you spend.

One of the most practical tools for budget-conscious shoppers is Amazon. Beyond just convenience, it offers something deeply valuable for anyone following the 50/30/20 rule: the ability to compare, research, and make intentional purchases instead of impulse buys driven by retail shelf placement or in-store pressure.

Amazon — Budgeting Tools, Books & Smart Buys

For anyone serious about improving their financial life, Amazon is a genuine resource — not just a shopping site. Consider what’s available:

- Personal finance books that have transformed millions of lives — available digitally at low cost

- Budget planners, financial journals, and expense trackers (physical versions many people prefer over apps)

- Home organization tools that reduce impulse spending by keeping your living space functional

- Bulk household essentials that reduce your “needs” spending over time when bought strategically

- Study resources and courses for students investing in their earning potential

Smart buying = smarter saving. When you research purchases, read reviews, compare prices, and buy intentionally rather than emotionally — you spend less and get more. Amazon’s ecosystem makes that kind of deliberate shopping much easier than traditional retail.

For families especially, using Amazon for planned household purchases rather than convenience shopping can make a meaningful difference in how far the 50% needs budget actually stretches. Explore our curated budgeting tips for specific product categories worth considering.

Browse Amazon Finance & Budget Tools →* Affiliate disclosure: We may earn a small commission on qualifying purchases through our link, at no additional cost to you.

Tools & Resources to Make Budgeting Easier

The 50/30/20 rule is simple by design, but the right tools remove friction and make it effortless to maintain. Here are genuinely useful options across different needs and preferences:

Free Budget Tracking Apps

YNAB (You Need A Budget) — arguably the most effective budgeting app in existence, built around intentional spending. Mint — auto-categorizes spending from connected accounts, great for seeing patterns quickly. Google Sheets or Excel — for those who prefer manual control and full customization. A simple three-column sheet for Needs, Wants, and Savings is all you need.

Books Worth Reading

All Your Worth by Elizabeth Warren (the origin of this rule). The Total Money Makeover by Dave Ramsey for aggressive debt payoff strategies. I Will Teach You To Be Rich by Ramit Sethi for automation-focused personal finance. The Psychology of Money by Morgan Housel for understanding the behavioral side of wealth. All available through Amazon at accessible price points.

Automation Tools

Most banks now allow automatic transfers on a set schedule. The moment your salary arrives, automate a transfer of 20% to a separate savings or investment account. Remove the decision entirely. Read more about building a complete financial system in our passive income ideas guide — because savings is only the first step.

The Most Powerful Tool: Pen and Paper

Don’t underestimate the physical act of writing your budget. Research consistently shows that people who write their financial goals and budget by hand have significantly better follow-through than those who only use apps. A simple notebook dedicated to your finances — monthly income, three category totals, monthly review notes — can be more powerful than any app. Consider a proper budget planner journal for a structured format.

Frequently Asked Questions

This is more common than the rule suggests, especially in high cost-of-living areas. If your needs are genuinely 55–65% of income, don’t abandon the framework — adjust it. Reduce your wants category first (to 20% or less), protect at least 10–15% for savings, and make increasing income a specific, active goal. The ratios are guidelines; the principle (intentional allocation, protecting savings) is non-negotiable.

Minimum debt payments (like a minimum credit card payment) fall under Needs — they’re non-optional. Any extra debt repayment beyond the minimum is considered part of your 20% savings category, since paying down debt is financially equivalent to earning a guaranteed return equal to your interest rate. If you’re carrying high-interest debt, it often makes sense to direct most of your 20% toward eliminating it before investing.

Yes, with one adjustment. Base your budget on your lowest reliable monthly income, not your average or best month. In higher-income months, direct the extra directly to savings. This creates a smoothing effect and prevents lifestyle inflation from consuming your good months.

Start by tracking your spending for one month without changing anything. Just observe. Then categorize everything you spent into Needs, Wants, and Savings/Debt. See what percentage each represented. That honest picture is your starting point. From the next month, set your targets and adjust. Read our complete financial planning guide for beginners for a more detailed walkthrough.

20% is an excellent starting point and better than what most people save. However, if your goal is early financial independence or significant wealth accumulation, consider working toward 25–35% once your income allows it. The 50/30/20 rule isn’t a ceiling — it’s a floor. Start at 20%; as your income grows, resist expanding your wants proportionally and direct the difference toward savings instead.

Savings includes: emergency fund contributions (until you have 3–6 months of expenses set aside), retirement account contributions, investment accounts, and extra debt repayments beyond minimums. Broadly: anything you’re setting aside for future financial security or growth counts as savings in this framework.

Absolutely — and it’s often more powerful when done together. Combine your after-tax household income and apply the rule to the total. Have an honest monthly review conversation. Couples who budget together tend to have significantly less financial conflict and better long-term outcomes. The key is shared transparency, not one partner controlling the budget.

Conclusion: Your Financial Story Starts Now

Here’s what nobody tells you about personal finance: it’s not really about money. It’s about freedom. The freedom to say yes to what matters. The freedom to say no to a job that doesn’t respect you. The freedom to handle the unexpected without panic. The freedom to give generously when it matters.

The 50/30/20 rule won’t make you rich overnight. Nothing will. But it will do something far more valuable: it will make you intentional. And intentionality, practiced consistently over years, is the actual engine of financial freedom.

You don’t need a finance degree. You don’t need a big salary. You need three numbers — 50, 30, 20 — and the discipline to honor them month after month, adjusting when life demands it, staying honest when you stray from it.

Start where you are. Not when the salary is higher, not after the next raise, not when life is less complicated. Life never becomes less complicated. Start now.

If this guide helped you, explore more of our resources: our budgeting tips library, our guide on how to save money fast, our complete financial planning guide, and ideas for building passive income once your budget foundation is solid.

Your future self is counting on the decision you make today.