How to Calculate Your Net Worth: Step-by-Step Guide for Beginners

How to Calculate Your Net Worth: Step-by-Step Guide for Beginners

Most people have a general sense of how much money they earn. Far fewer know their actual net worth.

This is a problem — because your income tells you how much money flows in each month, but your net worth tells you where you actually stand financially. It is the most complete single number that reflects your overall financial health.

Knowing your net worth is the starting point for every meaningful financial goal: getting out of debt, building savings, working toward financial independence, or understanding how your financial situation is actually changing over time.

This guide will explain exactly what net worth is, how to calculate yours step by step, what the number means, and what to do with it.

What Is Net Worth?

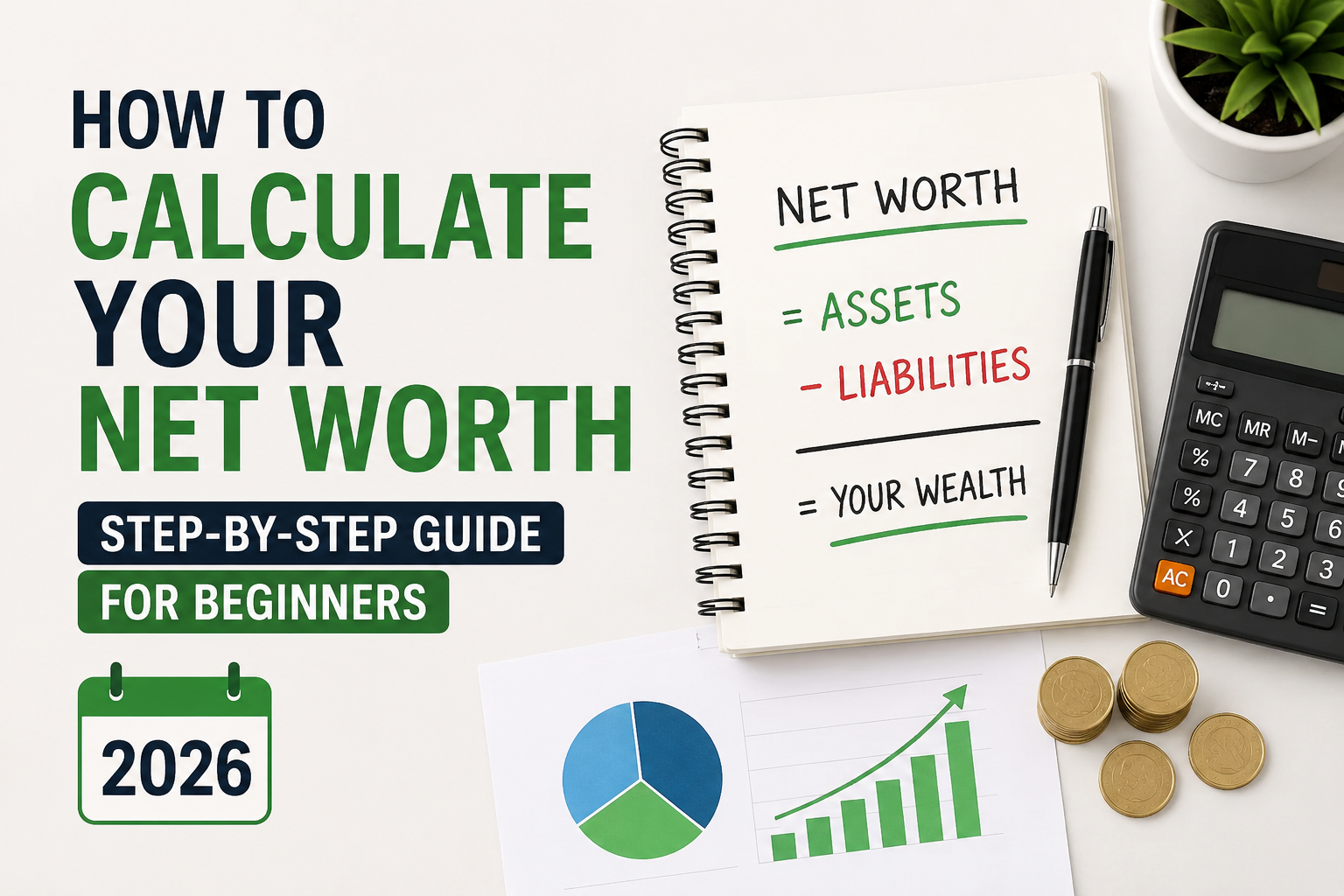

Net worth is the total value of everything you own minus the total of everything you owe.

Net Worth = Total Assets − Total Liabilities

- Assets = Everything you own that has monetary value

- Liabilities = Everything you owe to others

The result can be positive or negative. A positive net worth means your assets exceed your debts. A negative net worth means your debts exceed your assets.

Neither result is permanent. Net worth is a snapshot — and what matters most is whether it is trending in the right direction over time.

Why Your Net Worth Matters More Than Your Income

Income is important. But two people earning the same salary can have dramatically different financial situations.

Person A: Earns $60,000/year, saves 20% consistently, has minimal debt, and has been investing for 10 years. Net worth: $180,000.

Person B: Earns $60,000/year, spends everything, carries $30,000 in credit card debt, and has no savings. Net worth: −$15,000.

Same income. Completely different financial realities.

Net worth captures the cumulative result of all your financial decisions — spending, saving, investing, borrowing — not just what arrived in your bank account this month. That is why it is the more meaningful number for assessing long-term financial progress.

Step 1: Calculate Your Total Assets

Assets are everything you own that has real monetary value. List every single one.

Liquid Assets (Cash and Near-Cash)

These are assets you can access quickly:

- Cash on hand

- Checking account balances

- Savings account balances

- Money market accounts

- Cash value of any life insurance policies

Investment Assets

- Stocks, bonds, and mutual funds in brokerage accounts

- Index fund ETF holdings

- Retirement accounts (401k, IRA, pension value, or equivalent in your country)

- Cryptocurrency holdings (at current market value)

For building your investment assets, see: How to Invest With Little Money: Start With $100 or Less and Index Funds for Beginners: Complete Guide

Real Assets

- Primary home (current market value, not what you paid for it)

- Rental or investment property (current market value)

- Land

Personal Property

- Vehicle(s) — use current resale value, not purchase price

- Valuable jewelry or watches (at resale value, not retail)

- Collectibles with established resale value

- Business ownership stake (if applicable)

Important: Use current realistic market values, not emotional or sentimental values. Your car is worth what you could sell it for today — not what you paid for it three years ago.

Step 2: Calculate Your Total Liabilities

Liabilities are everything you owe to anyone. Include every debt, even small ones.

Short-Term Liabilities

- Credit card balances (all cards)

- Personal loan balances

- Medical debt

- Any money owed to family or friends

Long-Term Liabilities

- Mortgage balance (remaining amount owed, not original loan)

- Car loan balance

- Student loan balance

- Home equity loan or line of credit

- Business loan (if personally guaranteed)

Do not forget: Even debts you are “ignoring” or have not paid in a while are still liabilities until legally discharged.

For strategies to eliminate these liabilities: How to Get Out of Debt Fast in 2026 and Debt Snowball vs Debt Avalanche

Step 3: Do the Calculation

Once you have your two totals:

Net Worth = Total Assets − Total Liabilities

Example:

| Assets | Value |

|---|---|

| Checking account | $2,500 |

| Savings account | $8,000 |

| Investment account (index funds) | $22,000 |

| 401(k) retirement account | $35,000 |

| Car (resale value) | $12,000 |

| Total Assets | $79,500 |

| Liabilities | Balance |

|---|---|

| Credit card A | $4,200 |

| Credit card B | $1,800 |

| Car loan | $8,500 |

| Student loan | $18,000 |

| Total Liabilities | $32,500 |

Net Worth = $79,500 − $32,500 = $47,000

This person has a positive net worth of $47,000. They have more assets than debts.

What Is a Good Net Worth?

This is one of the most common questions — and the most honest answer is: it depends heavily on your age, income, country, and life stage.

A 25-year-old with a net worth of $5,000 is doing well if they recently graduated with student loans. A 45-year-old with a net worth of $5,000 faces a different situation.

One widely referenced guideline (from The Millionaire Next Door by Thomas Stanley and William Danko) suggests a target net worth based on income and age:

Target Net Worth = (Age × Annual Pre-Tax Income) ÷ 10

This is a rough benchmark, not a rule. Many factors — cost of living, career stage, country, family obligations — affect what is realistic.

What matters most is not a specific number but the direction of travel: is your net worth growing consistently over time?

What a Negative Net Worth Means

A negative net worth means your liabilities exceed your assets. This is common — and it does not mean you are in a hopeless situation.

Many recent graduates have negative net worth because of student loans. Many first-time homeowners have negative or near-zero net worth in the early years of a mortgage.

Negative net worth becomes a serious concern when:

- It is growing (debts increasing faster than assets)

- High-interest consumer debt (credit cards) is a major component

- No savings or investment assets exist

If your net worth is negative, the priorities are clear: eliminate high-interest debt first, build a small emergency fund, then begin building assets through saving and investing. See our complete guide: Build Wealth From Scratch: Saving, Investing & Smart Money Habits

How to Track Your Net Worth Over Time

Calculating your net worth once is useful. Tracking it over time is transformative.

When you see your net worth growing month after month — even slowly — it provides concrete evidence that your financial habits are working. When it drops, it signals something needs attention.

How to track it:

Free Spreadsheet Method

Create a simple spreadsheet with two columns — assets and liabilities — and update it monthly. Google Sheets or Excel both work well. This gives you full control and privacy.

Free Apps and Tools

Several free tools automatically connect to your accounts and calculate your net worth:

- Personal Capital (now Empower) — Comprehensive free dashboard connecting bank, investment, and loan accounts. Tracks net worth automatically.

- Mint — Free budgeting and net worth tracking (check current availability in your country)

- YNAB (You Need A Budget) — Paid tool ($14.99/month) with strong budget and net worth tracking

For a full breakdown of budgeting apps: Best Budgeting Apps 2026

Recommended frequency: Update your net worth monthly. Annual updates are too infrequent to catch problems early; daily updates create unnecessary anxiety.

How to Increase Your Net Worth

Your net worth grows in two ways: increasing assets or decreasing liabilities. The fastest progress usually comes from doing both simultaneously.

Increase Assets

1. Invest consistently. The most powerful way to build assets over time is consistent investing in low-cost index funds. Even small monthly contributions compound significantly over years.

For how to start: How to Invest With Little Money

2. Build your emergency fund. Liquid savings are assets. A funded emergency fund protects your other assets by preventing you from going into new debt for unexpected expenses.

For building yours: How to Build an Emergency Fund in 2026

3. Increase income. Higher income, when not matched by higher spending, generates more assets. Side income, salary negotiation, and skill development all contribute.

For ideas: Passive Income Ideas 2026

Decrease Liabilities

4. Eliminate high-interest debt aggressively. Every dollar of credit card debt paid off is a direct increase to net worth — plus it eliminates future interest costs. Prioritize the highest-interest debts first.

For strategy: Debt Snowball vs Debt Avalanche

5. Avoid new consumer debt. Taking on new debt — especially for depreciating assets like cars or consumer goods — immediately reduces net worth and adds ongoing interest costs.

6. Make extra mortgage payments (if applicable). Additional principal payments on a mortgage directly increase your home equity, which increases net worth.

The Wealth-Building Formula

The core formula for growing net worth is straightforward:

Earn more than you spend. Invest the difference. Eliminate debt. Repeat.

Every financial tool — budgeting, debt payoff strategies, investing — is in service of this fundamental formula.

Net Worth and Inflation — An Important Connection

One subtlety of net worth tracking: inflation affects the real value of both assets and liabilities over time.

If your net worth grows 3% per year but inflation is running at 4%, your real net worth — your actual purchasing power — is declining.

This is another reason why investing is essential to genuine wealth building, not just saving. Assets invested in inflation-beating vehicles (like broad stock market index funds) grow faster than inflation. Cash sitting in low-interest accounts does not.

For a full understanding of how inflation affects your financial position: What Is Inflation and How Does It Steal Your Money?

Net Worth Calculation Worksheet

Use this to calculate yours right now:

ASSETS

| Asset Category | Your Value |

|---|---|

| Cash (checking + savings) | $ |

| Investment accounts | $ |

| Retirement accounts | $ |

| Crypto holdings | $ |

| Home value (if owner) | $ |

| Vehicle(s) resale value | $ |

| Other valuable assets | $ |

| TOTAL ASSETS | $ |

LIABILITIES

| Liability | Balance Owed |

|---|---|

| Credit card(s) | $ |

| Personal loans | $ |

| Car loan | $ |

| Student loans | $ |

| Mortgage (remaining) | $ |

| Other debts | $ |

| TOTAL LIABILITIES | $ |

NET WORTH = Total Assets − Total Liabilities = $________

People Also Ask

Q: What is net worth in simple terms? Net worth is everything you own minus everything you owe. It is calculated by adding up all your assets (savings, investments, property, vehicles) and subtracting all your debts (loans, credit cards, mortgage balance). The result is your net worth.

Q: Is it good to have a high net worth? A higher net worth generally represents greater financial security and more options. However, what constitutes “good” depends on your age, income, country, and life stage. The more important question is whether your net worth is trending upward consistently.

Q: What should my net worth be at 30? There is no universal answer. A commonly cited rough benchmark is annual income multiplied by your age divided by 10. For a 30-year-old earning $50,000, that suggests a benchmark of around $150,000 — but this varies enormously based on career, student loans, housing, and other factors. The trend matters more than any specific target.

Q: Can I have a high income and low net worth? Absolutely. High earners who spend all their income, carry significant consumer debt, and do not invest can have very low or negative net worth. Net worth reflects cumulative financial decisions, not just current earnings.

Q: How often should I calculate my net worth? Monthly tracking is ideal — frequent enough to catch trends early, not so frequent it creates anxiety. At minimum, calculate your net worth quarterly.

Q: Should I include my home in my net worth? Yes. Your home’s current market value is an asset. The remaining mortgage balance is a liability. Your home equity (value minus mortgage balance) contributes to net worth. Use realistic current market values, not what you paid for the home.

Q: How do I increase my net worth quickly? The fastest legitimate path involves simultaneously reducing liabilities (paying off high-interest debt aggressively) and increasing assets (investing consistently, building savings). There is no shortcut — but doing both simultaneously accelerates net worth growth significantly.

Q: Is a negative net worth bad? A negative net worth means liabilities exceed assets. It is common early in life — especially with student loans or early mortgages. It becomes a serious concern if it is growing, driven by high-interest consumer debt, or accompanied by no savings or investment activity.

Summary Table

| Step | Action |

|---|---|

| 1 | List all assets at current market value |

| 2 | List all liabilities at current balance owed |

| 3 | Subtract: Assets − Liabilities = Net Worth |

| 4 | Set up monthly tracking (spreadsheet or app) |

| 5 | Focus on growing assets and reducing liabilities each month |

| 6 | Check progress quarterly and adjust financial habits accordingly |

⚠️ Financial Disclaimer: This article is for educational and informational purposes only. Net worth benchmarks and guidelines mentioned are general reference points, not personalized financial targets. Individual financial situations vary significantly based on income, country, lifestyle, and obligations. This article does not constitute personalized financial or investment advice. Please consult a qualified financial advisor for guidance specific to your situation. Finzaro360.com does not provide personalized financial advice.

Conclusion

Your net worth is the most honest financial number you have. It does not care about your salary, your job title, or what you drive. It reflects the cumulative result of every financial decision you have made — spending, saving, investing, borrowing.

Calculating it for the first time can be uncomfortable, especially if the number is negative or lower than expected. But knowing the real number is always better than guessing — because you cannot improve what you do not measure.

Start with the worksheet in this article. Calculate your net worth today. Write it down. Then look at it again in 30 days.

Every month that number moves in the right direction, however slowly, is a month of real financial progress. That is what matters.

What to Read Next on Finzaro360

- Build Wealth From Scratch: Saving, Investing & Smart Money Habits

- Compound Interest Calculator: How It Works & Why It Changes Everything

- How to Invest With Little Money: Start With $100 or Less

- Debt Snowball vs Debt Avalanche: Which Method Works Best?

- How to Get Out of Debt Fast in 2026

- What Is Inflation and How Does It Steal Your Money?

- Best Budgeting Apps 2026

Write for Finzaro360

Are you a personal finance writer or financial educator? We publish expert guest posts on Finance, Crypto, AI Tools, and Online Earning. Visit our Write For Us page to submit your pitch and earn a quality dofollow backlink.

Published on Finzaro360.com | Category: Finance